Trump, Trade Deficits & the Dollar

- R. Christopher Whalen

- Mar 3

- 5 min read

March 4, 2025 | With the first State of the Union message from President Donald Trump Tuesday night, we’ve started to collect commentaries about the Trump Administration and the phrase “unintended consequences.” No, those tariffs and other policy changes made by the Trump Administration are quite intentional and deliberate. We’ll hear more about additional cuts and tariffs during the State of the Union message. Trump is playing hurry up offense and that is not likely to change anytime soon.

When Federal Housing Finance director nominee Bill Pulte focused on cost cutting (instead of releasing the GSEs from government control) during his confirmation hearing last week, that gave you a peek at the priorities in Trump II for housing. We expect to see layoffs at FHFA and the GSEs in coming weeks.

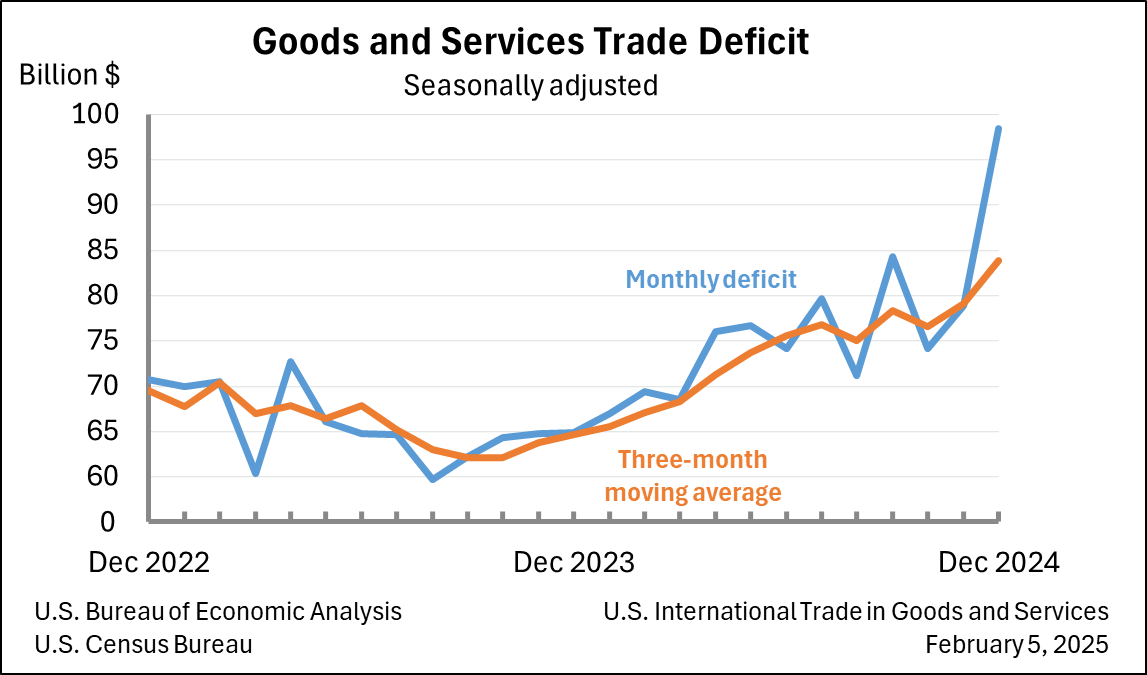

In Trump's executive order last month laying out his new administration’s priorities, “investigating the causes of our country’s large and persistent annual trade deficits in goods” was a lead item. Watching the abortive meeting between President Trump and Ukrainian leader Volodymyr Zelenskyy, we are reminded that most people still really do not understand the change that has occurred in Washington.

With the return of a purposeful, 19th Century conservative to the White House, President Trump is intent upon reversing the outflow of cash from the US to the rest of the world. This is a transcendental change that rejects the entire post-WWII era. But reducing the many deficits maintained by the US also means an equally dramatic change in the role of the dollar.

Trump likes to think of President Ronald Reagan’s legacy as a model for his political journey, but Reagan accepted the post-WWII global security consensus that Trump now explicitly rejects. You must go back to Senator Robert Taft or before WWI, to Teddy Roosevelt or even William McKinley, to capture the full measure of isolationist conservatism represented by Donald Trump.

Trump spurns the continuous state of war supported by both parties in Washington since 9/11, but also repudiates American economic and military support for allied nations going back to WWII. The America first orientation of Trump’s agenda is the most disruptive economic event since the victorious allies insisted on full payment of war reparations by Germany after WWI. The scale of the change is difficult for people to understand and accept as a given. But ultimately, President Trump measures success by how much deficits are reduced.

In order to deliver on the fiscal side, Trump armed with Elon Musk and DOGE will cut spending in all areas of government. In fact, Trump represents a dire threat to the entire global economy grown accustomed to ever rising US deficit spending. President’s Trump’s explicit goal is to reduce or even reverse the flow of dollars from the US to other nations. What does a sudden and sustained decrease in financial outflows mean for the world? How would a reduction in the $1.5 trillion trade deficit impact global GDP? Badly.

Contrary to what many hope, in fact the Trump encore may not be especially good for the corporate world. The steady migration of global CEOs through Mar-a-Lago seeking opportunities to appease the commander-in-chief describes the amount of money at stake in Washington under Donald Trump. As President Trump works, for example, to reduce the number of US military engagements around the world, he must also reduce the flow of dollars into and around the global economy and the defense sector.

Ponder the impact of DOGE terminating scores of contracts and leases throughout the federal government. Then extend this modern-day version of a Jacksonian, hard-money economics into a metaphor for fiscal probity around the world. Will Trump imitate President Andrew Jackson and require foreign nations to pay their tariffs in gold? Maybe. It's early yet.

When President Trump proposed for Ukraine to use its mineral resources to repay the United States $500 billion for military aid previously provided, he meant it. This reflects the Trumpian worldview that America should be repaid for its help – in full.

Many Americans who supported President Trump last November agree with the idea of other nations carrying the load and also want a reduced global role for America. This marks a radical departure from the model of America giving away billions of fiat dollars to other nations that has prevailed since WWII and especially in the Cold War.

As we note in our upcoming book “Inflated: Money, Debt and the American Dream,” most of the “loans” made by the US to other nations over the past century have defaulted or been forgiven. The reduction in US aid and, indeed, the imposition of tariffs on many nations will begin to reverse 75 years of economic hegemony for the US, a dominant role largely financed with borrowed money. How does the global role of the dollar look after a few years of American disengagement? Good question.

What is perhaps most interesting about the reprise of President Donald Trump is that predictions of doom and gloom for the US always focused on foreign nations losing their taste for dollars. But as we note in "Inflated," the global convenience of the dollar as a means of exchange is a free good exploited by the entire world. Nations can merely use dollars for trade, but invest reserve assets in other currencies.

Nobody is looking for a replacement for the dollar, at least not yet. But what happens if the US simply picks up the proverbial football and goes home? The growing unwillingness of the US to finance the global role of the dollar via external deficits and internal inflation is the new narrative that carried Donald Trump into office last November. Watching the world figure this out over the next year will be great entertainment and also fuel for a lot of market volatility.

Available May 2025!

The Institutional Risk Analyst (ISSN 2692-1812) is published by Whalen Global Advisors LLC and is provided for general informational purposes only and is not intended for trading purposes or financial advice. By making use of The Institutional Risk Analyst web site and content, the recipient thereof acknowledges and agrees to our copyright and the matters set forth below in this disclaimer. Whalen Global Advisors LLC makes no representation or warranty (express or implied) regarding the adequacy, accuracy or completeness of any information in The Institutional Risk Analyst. Information contained herein is obtained from public and private sources deemed reliable. Any analysis or statements contained in The Institutional Risk Analyst are preliminary and are not intended to be complete, and such information is qualified in its entirety. Any opinions or estimates contained in The Institutional Risk Analyst represent the judgment of Whalen Global Advisors LLC at this time, and is subject to change without notice. The Institutional Risk Analyst is not an offer to sell, or a solicitation of an offer to buy, any securities or instruments named or described herein. The Institutional Risk Analyst is not intended to provide, and must not be relied on for, accounting, legal, regulatory, tax, business, financial or related advice or investment recommendations. Whalen Global Advisors LLC is not acting as fiduciary or advisor with respect to the information contained herein. You must consult with your own advisors as to the legal, regulatory, tax, business, financial, investment and other aspects of the subjects addressed in The Institutional Risk Analyst. Interested parties are advised to contact Whalen Global Advisors LLC for more information.

Comentários